We've Got Mail!

While we started out in real estate investing and note investing many years ago, our goal was to make a profit from a business. What we didn’t completely realize in the beginning how much fun we’d have by helping others buy a home, sell a house, be able to stay in their home, invest in real estate, or in notes. We couldn’t fully comprehend that we would be making an impact on people’s lives.

I remember when we stood in a driveway of a house in Federal Way, Washington. Marishka and I had just met with a couple who lived just a few blocks from the house. We had just arrived at a solution as to how they could purchase the house. With a sob in his throat, and tears in his eyes, Ed said “You don’t know how much this means to me and my family.” They had lived in the neighborhood for 17 years, had always rented, and as a home remodeler for others, he hadn’t seen much hope to buying a home. With some creative terms and sweat equity, Ed and his family were able to move into and buy the home. The thought that we were able to help them still brings me pride joy.

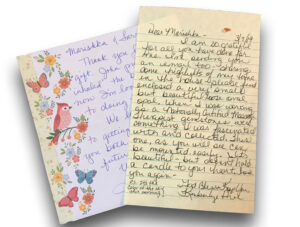

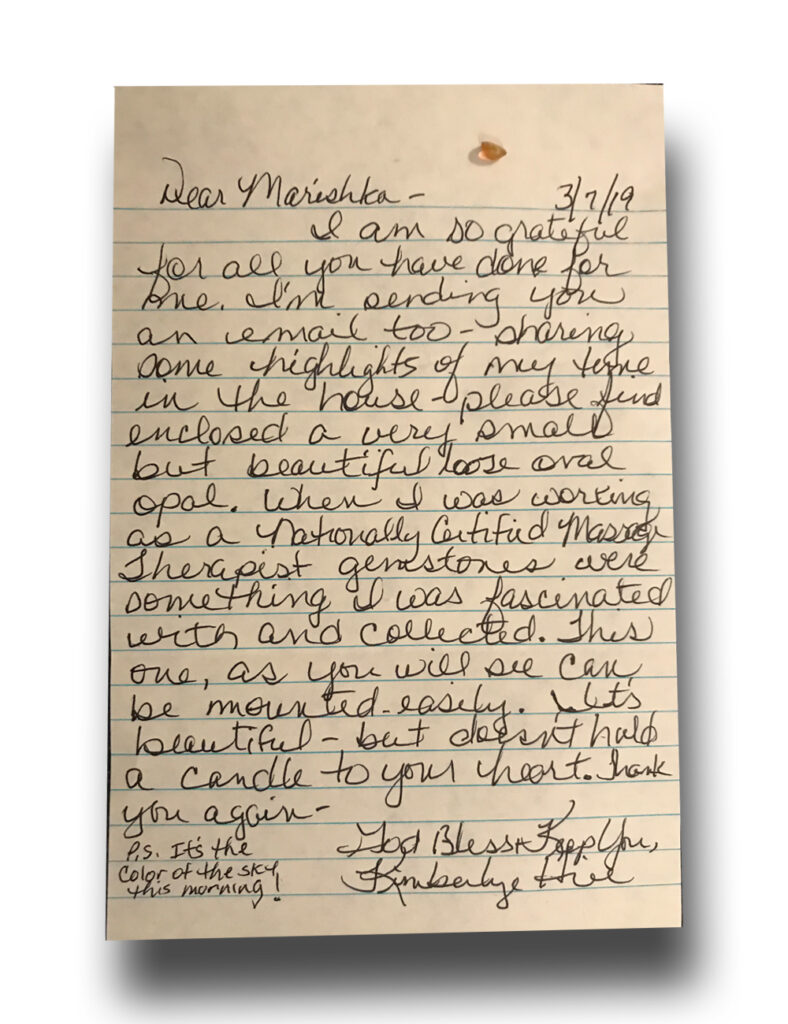

We get a lot of referrals and repeat business. We truly are blessed with the folks we are able to work with, and when we get a thank you note unexpectedly in the mail, it humbles and honors us that we’re able to help. I just wanted to share a couple of those notes. The first thank you is from a woman who could not afford to keep her house any longer. We were the lender on the home. By the way, Marishka is a saint. When it was apparent that the payments had stopped, Marishka spent hours on multiple phone calls with Kimberly, mainly listening to her in a patient and compassionate way. She gave her ideas on how she may be able to qualify for some assistance, or perhaps her daughter could purchase the house. In the end, Kimberly asked “Can I just give you back the house?” We did a deed in lieu of foreclosure so her credit would not be impacted. We send her the documents to sign and in the return envelope we received this very thoughtful thank you, along with a gem stone. To say the least, Marishka was in tears this time. A chapter in Kimberly’s life was closed and she was able to move on.

We get a lot of referrals and repeat business. We truly are blessed with the folks we are able to work with, and when we get a thank you note unexpectedly in the mail, it humbles and honors us that we’re able to help. I just wanted to share a couple of those notes. The first thank you is from a woman who could not afford to keep her house any longer. We were the lender on the home. By the way, Marishka is a saint. When it was apparent that the payments had stopped, Marishka spent hours on multiple phone calls with Kimberly, mainly listening to her in a patient and compassionate way. She gave her ideas on how she may be able to qualify for some assistance, or perhaps her daughter could purchase the house. In the end, Kimberly asked “Can I just give you back the house?” We did a deed in lieu of foreclosure so her credit would not be impacted. We send her the documents to sign and in the return envelope we received this very thoughtful thank you, along with a gem stone. To say the least, Marishka was in tears this time. A chapter in Kimberly’s life was closed and she was able to move on.

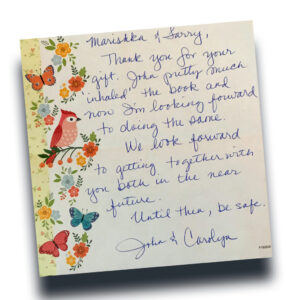

We love sharing books and resources that we’ve read and found valuable in our business. While note and real estate investing can be complicated and perhaps confusing, a book can sometimes help clear up some of the mystery. Feel free to ask if we have any favorite books to share.

5 Reasons Owners Offer Seller Financing

- Why would a seller allow a buyer to make payments over time for the purchase of property?

- Wouldn’t the seller rather get paid now and require the buyer to obtain a bank loan?

Here are 5 reasons property owners offer seller financing:

- Reduced Marketing Times

What is the first thing a real estate agent does when property is not moving and has been on the market for 60 to 90 days? They reduce the price and add the tagline “price reduced” to all advertising and signs. Rather than reduce the price, it might be beneficial for the seller to offer financing. Buyers provided with financing can certainly pay full price in exchange for the many benefits they receive with owner financing, including the money they save by not paying expensive loan fees, origination fees, and points.

- Increased Inventory of Prospective Purchasers

By offering owner financing, the seller increases marketability with a wider group of available purchasers. Statistics show that almost 40 percent of the American population is unable to qualify for traditional bank financing. While not all of the “unqualified” group would be an acceptable risk for owner financing, it still widens the market of prospective buyers considerably. Anyone who has added the words “Owner Will Finance” or “Easy Terms” to a For Sale ad or Multiple Listing Service (MLS) listing knows the phone will ring off the hook with interested prospects.

- Reduced Closing Times

Another advantage of offering owner financing is substantially lower closing times. A closing involving a third-party conventional lender can take six to eight weeks while closing a seller-financed transaction through a reputable title company can take as little as two to three weeks. This is due to the reduced paperwork and less restrictive due diligence process.

- Investment Strategy for Hard to Finance Properties

There are many properties that encounter financing difficulties including mixed use property, land, mobile and land, non-conforming, low value, and others. Investors realize excellent returns by paying a reduced cash or wholesale price on a hard-to-finance property and then reselling at a higher retail price with easy financing terms.

- Interest Income

Why let the banks earn all the interest? Sellers can keep the property-earning income even after they sell by offering owner financing. For example, a $100,000 mortgage at 9 percent with monthly payments of $804.62 will pay back $289,663.20 over 30 years. That additional $189,663.20 (over the $100,000 mortgage) is power of interest income!

Work with Owner Financing Specialists

If considering seller financing, be sure to consult with a qualified professional to properly document the transaction.

It also helps to speak with note investors to gain insight on appealing terms and structuring techniques. This assures top-dollar pricing should you ever want to convert the payments to cash by assigning your note, mortgage, deed of trust, or contract to an investor.

Say NO to Taxes!

A little understood IRS loophole in the US Tax Code could help you get top dollar for your property today – without you being on the hook for a giant tax bill.

Is This Too Good to Be True?

If you have been a property owner for any length of time, you have likely benefited from significant appreciation, and if you’re a landlord or investor you probably have taken advantage of numerous deductions as allowed by the IRS…

However, when you go to sell your property in the traditional way, you will be taxed on the gain — and those deductions will get recaptured — leaving you with a BIG TIME TAX BILL.

My team and I have perfected a way to sell your property that changes all that! We can help you get top dollar for your property today — and you won’t be left with a giant tax bill.

26 U.S. Code 453 – Installment method — Like to know more? Talk to us.

When Good Intentions Meet Predatory Practices

As real estate investors, we’ve all encountered situations where we genuinely want to help someone, but the numbers just don’t work. What breaks my heart is when these vulnerable homeowners fall prey to predatory operators who make promises they never intend to keep.

The Story

About two years ago, my business partner/husband Larry and I met a lovely elderly couple who responded to one of our marketing pieces. We met with them and we quickly learned their situation: they had purchased the home just a year earlier with a VA loan and had no equity. The reason they wanted to sell was heartbreaking – their daughter had stage 4 cancer, and they had moved in with her to help care for their grandchildren.

During our initial meeting at their kitchen table, we discussed their options thoroughly. The husband mentioned they had a timeshare they’d been paying on but couldn’t use. Larry offered to review the paperwork, made a few calls, and discovered this particular timeshare was easy to exit – they just needed to pay $200 in back dues and call a specific number to cancel. We provided this information at no charge, simply wanting to help reduce their financial burden.

Our Proposed Solution

Given that they had no equity and their monthly mortgage, taxes, and insurance exceeded market rent, a traditional wrap loan wasn’t viable. They wanted to keep the deed in their name, especially with him remaining on the mortgage, which we respected.

Our solution: a multi-year lease option that would give the market time to recover. We proposed starting with rent several hundred dollars below their monthly payment – they would subsidize the difference, but this was far better than their current situation of paying over $2,000 monthly out-of-pocket. We committed to increasing rent over time as market conditions allowed.

Anyone who knows us understands we’re not high-pressure salespeople. Perhaps we should be – in this case, it might have served this couple better.

The Predatory Alternative

While they were reviewing our paperwork, a wholesaler approached them with promises we knew were impossible to fulfill. They offered to buy the property “subject to” (meaning the couple would deed over the property but remain on the mortgage), promising $30,000 upfront and no more payments.

The husband contacted us about this offer. We sensed he was hoping we’d match it, but we couldn’t – while we try to help people, we don’t intentionally enter bad business deals, and there was no way this scenario would cash flow. I advised extreme caution, suggested they ask detailed questions, get attorney review, and explained why the offer seemed too good to be true. I don’t believe they followed this advice.

The Devastating Outcome

The wholesaler convinced them to sign. Over the following months, I watched local “agent-investors” I know promote this property at prices far above market value. Predictably, it didn’t sell.

When I checked on the couple several months later, they revealed they’d never received a penny from the company and were still making mortgage payments on a house they didn’t occupy. Worse, they couldn’t sell or lease the property because the deed was no longer in their name.

Yesterday, I received a heartbreaking call. The wife informed me that her husband had passed away last week. Despite everything that happened, she said they really liked us and trusted us, wanted me to know of his passing, and invited us to the service. My heart breaks for her and her family.

The Bigger Picture

Situations like this are exactly why distressed homeowner protection laws exist and why many states are cracking down on wholesalers and subject-to promoters. These strategies can be executed legally and ethically, but too many operators ignore both the law and basic ethics.

As legitimate real estate professionals, we have a responsibility to:

- Provide honest assessments, even when the numbers don’t work in our favor

- Educate homeowners about red flags in too-good-to-be-true offers

- Refer people to legal counsel when appropriate

- Maintain our integrity, even when it costs us deals

Key Takeaways for Homeowners

If you’re facing financial distress with your property:

- Be wary of any offer that seems too good to be true

- Always get a second opinion from a trusted advisor

- Have an attorney review any paperwork before signing away property rights

- Ask detailed questions about how promises will be fulfilled

- Verify the track record and credentials of anyone you’re considering working with

This business can be heartbreaking, but it’s stories like this that remind us why ethical standards matter. We may not be able to help everyone, but we can ensure we never contribute to someone’s financial devastation.

Beyond the business aspect, we genuinely care about the people we meet. That phone call yesterday was a powerful reminder that real estate isn’t just about properties – it’s about people and their lives.

What red flags have you encountered in distressed property situations? How do you maintain ethical standards while staying competitive in this market?